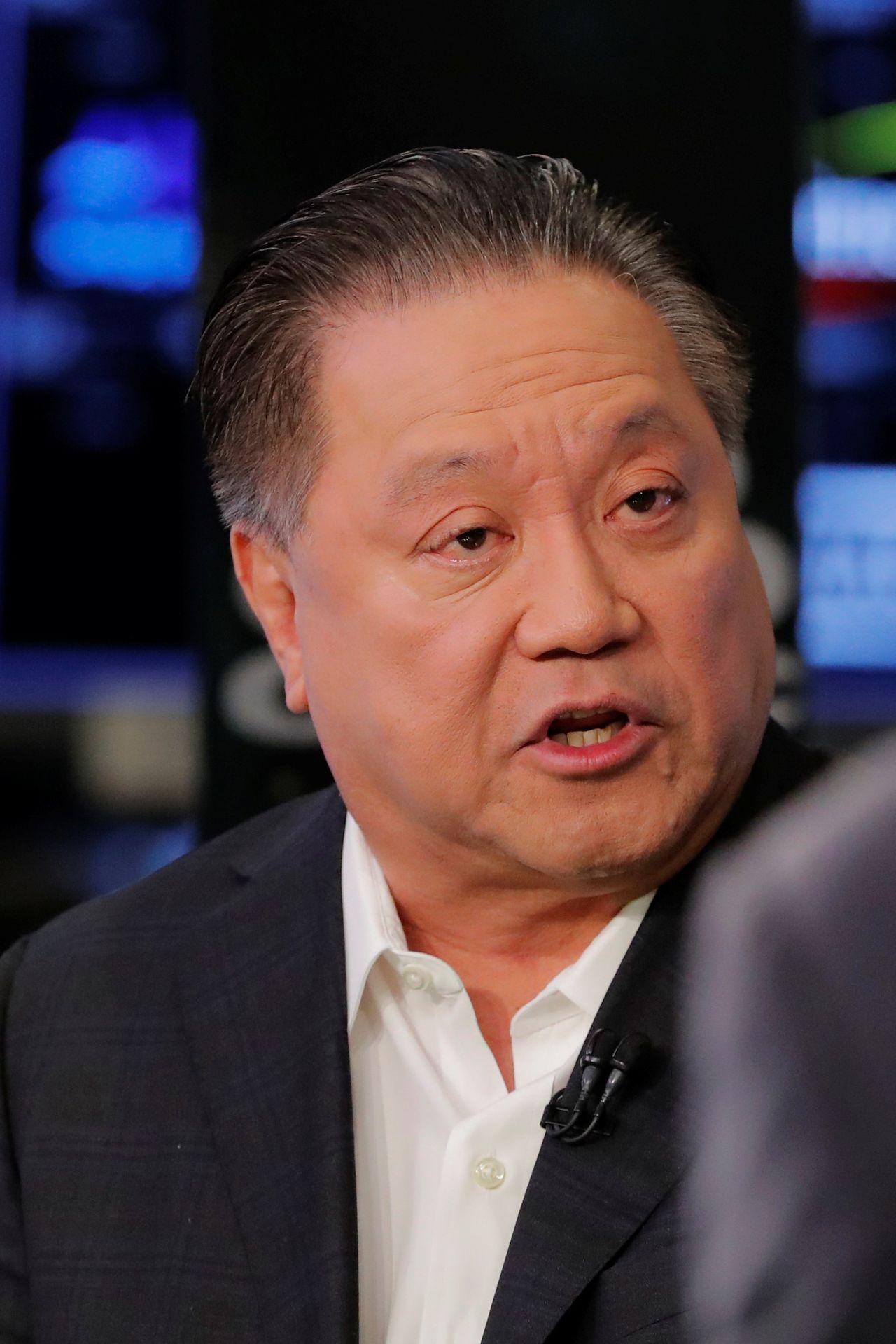

Broadcom Chief Executive Hock Tan shelled out $40,000 to sit at Xi Jinping’s table for the Chinese leader’s recent dinner in San Francisco with the heads of American businesses. Tan had a lot more at stake—a $69 billion deal he was waiting on China to approve.

For months, Chinese regulators wouldn’t clear the U.S. chipmaker’s bid to buy enterprise software developer VMware, leading Broadcom to put off its date for completion of the deal—first announced in May 2022—three times. Beijing had held up previous mergers involving U.S. companies. Intel’s planned acquisition of Israeli firm Tower Semiconductor, for more than $5 billion, was scuttled in August after Chinese regulators failed to approve it.

A few days after the dinner, China signed off on Broadcom’s deal. Beijing also gave a long-awaited green light to New York-based payments processor Mastercard to issue yuan-denominated cards bearing its brand in the country.

Some observers saw the moves as olive branches to American corporations as firms grow wary of doing business in China. The moves also show how companies can become pawns in the intensifying geopolitical competition between Washington and Beijing.

As recently as October, officials at China’s antitrust regulator, the State Administration for Market Regulation, indicated to Broadcom that they were ready to sign off on the deal as long as the company met all its conditions, according to people familiar with the matter.

Broadcom executives, however, extended the deal deadline after getting indications from Chinese officials that it wouldn’t be a simple business decision. China’s Foreign Ministry would have a say as well, the people said.

With that in mind, Broadcom’s Tan sought and succeeded in securing a spot in a meeting with Chinese Foreign Minister Wang Yi in late October, the people said. Wang, who was in Washington to pave the way for Xi’s November visit, held a meeting with U.S. business leaders on the sidelines of his trip.

During the session, Tan, an ethnic Chinese businessman born in Malaysia who is now an American citizen, raised the Broadcom-VMware deal. Wang responded by saying Beijing continued to welcome foreign investment, without giving any clues to China’s possible actions, the people said.

Broadcom declined to comment. Mastercard didn’t respond to questions. China’s foreign ministry referred The Journal to the official statement released on Nov. 21 approving the Broadcom deal.

The approvals for Mastercard and Broadcom are isolated successful cases and must be viewed in the context of the bilateral relationship, said Eric Zheng, the president of the American Chamber of Commerce in Shanghai, whose members have cited uncertain U.S.-China ties as their biggest concern operating in the country.

“These should be standard business practices, based on established laws and regulations,” Zheng said in an interview. “Foreign businesses want such events not to be politicized.”

China has long used access to its huge consumer market as a tool to eke out geopolitical and business concessions. More recently, it has leveraged its access to raw materials such as critical minerals and used antitrust approvals to hit back at trade actions it views as unfavorable. Chinese officials also feel frustrated by U.S. actions that Beijing views as unfairly punishing Chinese companies.

Broadcom, Mastercard and Boeing were among the underwriters of the dinner for Xi hosted by American business groups.

While Mastercard was granted access it had been seeking for years, U.S. plane maker Boeing is still frozen out.

China hasn’t bought passenger planes from Boeing since 2017, amid trade tensions between the two nations and two fatal crashes of Boeing’s 737 Max passenger jet. No resumption had been announced as of Monday, despite the hopes of some investors after Xi’s cordial summit with Biden that helped take the heat out of rising tensions between the world’s two biggest economies. Xi’s dinner with American leaders—including Merit Janow, chair of Mastercard’s board of directors—left many disappointed over the lack of talk about trade.

Boeing declined to comment.

Many business executives caution that recent approvals are unlikely to open the investment floodgates into China, and Beijing has much to do to convince multinationals that they are welcome there.

A poll released by New York-based think tank the Conference Board on Thursday shows chief executives of multinational companies are becoming less confident about China as economic woes in the country persist.

The survey of 35 China-based CEOs of mostly U.S. and European companies, conducted before the recent approvals, shows that a measure of their confidence in China dropped from 72 six months ago to 54 in the second half of the year. A reading of below 50 points reflects more negative rather than positive responses.

The think tank also found that 40% of CEOs expected a decrease in capital investments and almost as many forecast a reduction in head count over the next six months, up from just 9% in the first half of the year.

Overseas firms withdrew more than $160 billion in total earnings from China in the six successive quarters through the end of September, Chinese data show, an unusually sustained run of profit outflows illustrating the decline in the country’s appeal for overseas capital.

Several challenges facing American businesses in China remain from opaque data localization laws to shrinking access to information within the country. Raids on foreign due diligence and consulting firms, including the detention of staff, and exit bans on executives have also made companies nervous about their presence there. Also, doing business there can draw scrutiny from officials and lawmakers in Washington.

“It is a carrots and sticks operating environment, and we appear to be in the carrots mode,” James Zimmerman, a partner at Perkins Coie LLP, who counsels foreign companies on corporate and regulatory issues in China, said.

“China is an operating environment where every license, permit and approval is a process that can become highly politicized, and more so when U.S.-China relations go south,” he said.

Write to Lingling Wei at [email protected] and Liza Lin at [email protected]

News Related-

Russian court extends detention of Wall Street Journal reporter Gershkovich until end of January

-

Russian court extends detention of Wall Street Journal reporter Evan Gershkovich, arrested on espionage charges

-

Israel's economy recovered from previous wars with Hamas, but this one might go longer, hit harder

-

Stock market today: Asian shares mixed ahead of US consumer confidence and price data

-

EXCLUSIVE: ‘Sister Wives' star Christine Brown says her kids' happy marriages inspired her leave Kody Brown

-

NBA fans roast Clippers for losing to Nuggets without Jokic, Murray, Gordon

-

Panthers-Senators brawl ends in 10-minute penalty for all players on ice

-

CNBC Daily Open: Is record Black Friday sales spike a false dawn?

-

Freed Israeli hostage describes deteriorating conditions while being held by Hamas

-

High stakes and glitz mark the vote in Paris for the 2030 World Expo host

-

Biden’s unworkable nursing rule will harm seniors

-

Jalen Hurts: We did what we needed to do when it mattered the most

-

LeBron James takes NBA all-time minutes lead in career-worst loss

-

Vikings' Kevin O'Connell to evaluate Josh Dobbs, path forward at QB